7 Easy Business Concepts Every Founder Needs To Know

By Kayleigh Alexander

Over 500,000 new businesses are set up every month, but only half manage to get to the five year mark, a statistic that can be a little alarming if you’re thinking of founding one of your own.

The infancy period of any start-up is volatile, and it can be especially difficult for entrepreneurs who don’t have any previous business experience.

Having a grip on some basic business concepts will give you some of the tools you need to successfully establish your brand and then keep it growing. Don’t blindly fight against established business norms — learn them, boss them, and then choose to subvert them if you want.

Here are seven easy business concepts that you need to know to help you realize your wildest creative business dreams.

Competitive advantage

One of the main challenges for young businesses is finding a way to achieve and maintain a competitive advantage over other brands in a given market.

Put simply, a competitive advantage is an advantage you have over your competitors. This is achieved by giving your customers greater value — either by offering lower prices or justifying higher prices by providing a better product or service.

In his 1985 book ‘Competitive Advantage’, Harvard Business School professor Michael Porter outlined three core ways that businesses can achieve a sustainable competitive advantage:

● Cost leadership means providing reasonable value at a lower price, which can be done by improving operational efficiency. Basically doing more with less — gig economy businesses are great for this

● Differentiation means delivering greater benefits to the customer than your competitors can. This can typically be achieved through having an innovative product, a very high-quality product, or delivering a similar product as your competitors, but offering exceptional customer service. Differentiation is often how creative businesses like yours stand out

● Focus means that the company’s founders understand and serve their target market better than its competitors. The key to focusing is to choose one specific target market, often a niche that bigger companies don’t serve, and then concentrating hard on nailing it.

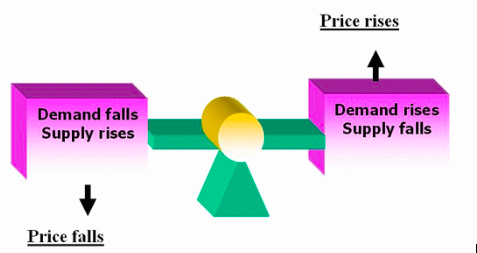

Supply and Demand

The concept of supply and demand is directly relevant to any company competing in the marketplace, regardless of its size. Supply and demand mean that a market will respond to changes in demand and supply to overcome surplus and shortages and therefore maintain an ‘equilibrium price’. For example, a shortage of gold leads to a higher price, because, as demand for gold increases, the upward pressure on prices would naturally prevent a shortage.

Source: The Dasinger Daily

Understanding the specific supply and demand issues affecting both the sales and the purchases that your business makes will enable you to make more informed decisions.

Return on Investment

Return on Investment (ROI) is the financial benefit that is received from an investment, or, put more simply, a measure of what you get back compared to what you put in. For example, say you spent $1000 per month on Google Adwords, and your business made $2000 as a direct result of the ads, your ROI would be the difference. ROI is usually measured as a ratio, which in this case would be 2:1, because for every $1 you spend, you get $2 back.

Calculating ROI will help you to track what’s working and what isn’t working for your business. If your ads aren’t generating a profit, you will know that you need to make changes to them, or drop them altogether in favor of another form of marketing.

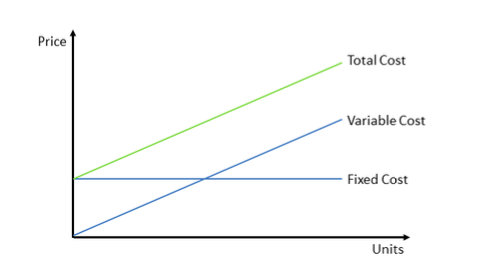

Fixed and Variable Costs

When you start a business, your costs come in two forms: fixed and variable. Fixed costs don’t change when your sales volume changes, but variable costs do. Examples of fixed costs include the rent you pay for the space that your company uses, such as an office or storage facility, insurance, marketing and management salaries. Examples of variable costs are material and labor, the costs of which go up and down depending on sales.

Source: PrepLounge

Understanding which costs are fixed and which are variable will enable you to budget and plan accordingly, and help you to identify what is a profitable price level for your products or services. If you suddenly lost your biggest customer account and therefore 25% of your sales, you’d still need to cover your fixed costs to keep your company running; figuring out these costs could be crucial to keeping your company alive.

Customer Lifetime Value

Customer Lifetime Value (CLV) is the total worth of a customer to a business over the entirety of their relationship. It’s important to your business because it costs less to keep existing customers than it does to acquire new ones. According to the book Marketing Metrics, “businesses have a 60-70% chance of selling to an existing customer, whilst the probability of selling to a new customer is only 5% to 20%”. Increasing the value of your existing customers will really help to drive growth.

However, measuring CLV isn’t easy, with only 42% of companies feeling able to do it, and citing poor systems, lack of coherent marketing and lack of integration as the reasons why.

If big, established businesses struggle to measure CLV, then new and small businesses are likely to find it hard to make accurate measurements, but you can make a start with this simple formula: customer revenue minus the cost to acquire and serve the customer. If you are prepared to really drill down into the concept, there are more complex calculations that will help you get a more accurate result.

Customer Acquisition Cost

Customer Acquisition Cost (CAC) means the price that your business pays to acquire a new customer. It can be worked out by dividing the total costs associated with acquisition by total new customers, within a specific time period. For example, if you spend $500 on marketing in one month and acquire 500 customers, then your CAC is $1. Web-based companies can roll out highly targeted campaigns and track customers from leads to conversions, making their CAC highly accurate.

If you’ve just started a business, acquiring customers is crucial to making sure it is a success, but if you spend too much money on acquiring customers, then you won’t be able to pay your other costs and keep your business afloat. CAC is directly relevant to CLV, and combining the two will allow you to calculate what is the true value of a customer to your business.

Minimum Viable Product

Minimum Viable Product (MVP) is a development technique where a new product is introduced to the market with basic features, which will capture the attention of early adopters. Companies such as Uber, Dropbox, and Airbnb all started as MVPs and achieved very rapid growth. An MVP is a bare-bones version of a product that includes a minimum of features and directly addresses the core problem it is trying to solve. Once the initial product is successful, more features can be added.

Source: Cheesecake Labs

An MVP allows you to release your product to market in the shortest possible time, reduce start-up costs and test demand before spending money adding all the bells and whistles.

An easy creative product-based MVP would be a print-on-demand business with low overheads. Simply set up shop, hook up with an app like Printful, and go out looking for ways to make your first sale. Using print-on-demand methods means you can keep costs of production down while you test your designs and brand out with your target market.

On the service side, you might be looking to start a consultancy coaching business for creative entrepreneurs. Before going all-out, test the waters with a series of blogs, a webinar, or a training course (Thinkific is good for this) to gauge whether you have a viable market and compelling message. You may find that you need to adapt your messaging.

You can work directly with users to analyze behaviors and get feedback, allowing you to develop your product in ways that you know customers will like. Developing your business in this way can also avoid large capital losses, therefore attracting potential investors because it is a low-risk venture.

There’s a lot to learn when setting up a new business and there is no guarantee of success, but educating yourself about some of the basic principles will stack the odds in your favor. A firm grounding in everything from basic economic theory such as supply and demand to sophisticated development techniques like MVP will help you found a business that is both profitable and sustainable.

Kayleigh Alexandra is a content writer for Micro Startups — a site dedicated to giving through growth hacking and shining a light on innovative startups. Visit the blog for your latest dose of startup, entrepreneur, and charity insights from top experts around the world. Follow us on Twitter @getmicrostarted.